Whether you're a first-time buyer or moving home, if you're looking to get a mortgage, it's important you get up-to-speed with the Central Bank’s mortgage lending rules.

The Central Bank’s mortgage lending rules were introduced back in 2015 and have fundamentally changed the mortgage landscape in Ireland.

The rules dictate how much you're allowed borrow for a mortgage in relation to your income, as well as how much you must have for a deposit, and are designed to ensure that financial institutions lend money sensibly.

Under pressure from both the banking industry and government for the rules to be loosened, the Central Bank amended the rules in 2022 following an in-depth review.

What are the Central Bank’s mortgage lending rules?

There are two main rules that you need to be aware of:

1. Loan-to-income limit

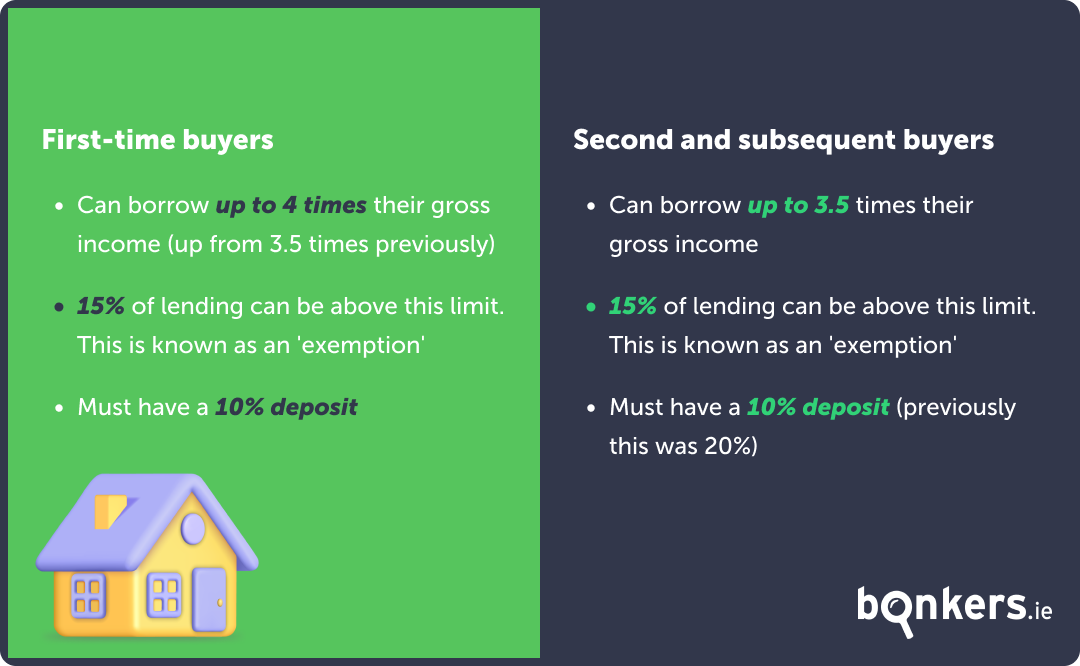

The Central Bank's rules limit the maximum amount someone can borrow. This is four times your gross annual income if you're a first-time buyer and 3.5 times your gross annual income if you're a second-time or subsequent buyer.

The same rules apply regardless of how much you earn.

So let's say, for example, that you're on a salary of €50,000 a year. This means you're allowed borrow a maximum of €200,000 under the Central Bank's rules if you're a first-time buyer. If you’re buying with a partner who also earns €50,000, that amount doubles to €400,000.

If you're a second-time buyer and you earn €50,000 a year you can only borrow €175,000.

2. Loan-to-value ratio

The second mortgage lending rule relates to the loan-to-value ratio that lenders are required to observe. This refers to the percentage of the property’s value that you can borrow and how much of it you must pay for upfront in the form of a deposit.

It's often simply called "the deposit rule".

First-time buyers and second-time or subsequent buyers are allowed a maximum loan-to-value of 90%, meaning you're required to have a deposit of at least 10% for any property.

Let's say, for example, that you're a first-time buyer and you want to buy a house for €300,000. The rule means you'll need a minimum deposit of €30,000 before you can be lent the remaining €270,000.

What is meant by income?

Some people also receive social welfare payments, commission, bonuses and other sources of income in addition to their regular monthly or weekly wage.

Lenders will also take this income into account when deciding how much they can lend you under the Central Bank's loan-to-income rule. But all the lenders view these sources of income slightly differently, meaning you may be able to get a slightly bigger mortgage with one lender over the other.

If you apply for a mortgage with a broker like bonkers.ie, we'll be able to tell you which lender will offer you the biggest mortgage for your particular circumstances.

Exceptions to the rules

In any one calendar year, 15% of mortgages that lenders give out to first-time buyers can breach the income limit or the deposit requirement. And 15% of mortgages given to second time or subsequent buyers can breach the rules.

There are often called "exemptions".

With an exemption a mortgage seeker can potentially borrow up to around 4.75 times their income.

However, banks don't always use up their full quota of exemptions. So just because they're available it doesn't mean you'll get one.

How do I get a mortgage exemption?

Firstly, you need to know that you can usually only get an exemption under ONE of the lending rules. It's extremely rare that a bank will allow you to breach both the loan-to-income limit as well as the loan-to-value ratio. It's either one or the other.

Whether you get an exemption will depend on your credit worthiness, the quality of your mortgage application and whether the lender still has room to give out an exemption.

Exemptions are often all used up by the middle of the calendar year, so if you want to apply for one, the earlier in the year that you apply for your mortgage the better.

Banks will usually only give a mortgage exemption to people in professional jobs who are on higher incomes, which is around €60,000 or above for a single applicant and €80,000 and above for a joint application.

Some banks are much more likely to offer an exemption than others. And not all will offer up to 4.75 times your salary — some will only offer a maximum of 4.5 times. And your chances of getting approved for an exemption are higher if you go through a mortgage broker.

A limit, not a guarantee

It's important to remember that the Central Bank's lending rules only refer to the maximum amount you can be lent.

Banks will take into account your other loans, outgoings, bills and commitments before deciding how much they will lend you.

For more information, see our guide on how mortgage applications are assessed

Do the Central Bank's mortgage lending rules apply to switchers?

If you're thinking of switching your mortgage then the Central Bank's rules don't apply. However most banks won't let you switch if you're in negative equity and most will require you to have at least 10% equity in your home.

Do other countries have these rules?

Yes. Ireland is not alone in having these types of rules.

Many other countries in Europe have rules which dictate how much you're allowed borrow for a mortgage and how much of a deposit you need. And in some cases the rules are even stricter than ours.

What now?

So, now that you know how much you're allowed to borrow in theory, what next?

In order to avoid becoming bamboozled during meetings with your bank or mortgage broker, it’s a good idea to familiarise yourself with some of the mortgage-related buzzwords you're likely to come across in your mortgage journey.

- Check out this guide to learn about the various types of mortgage interest rates.

- If you’re a first-time homebuyer you could claim a tax rebate of up to €30,000 with the Help-to-Buy scheme, which is designed to help first-time buyers acquire the deposit necessary to buy a newly built home.

- Fixed mortgage interest rates have become increasingly popular, however it’s important to understand the pros and cons of both variable and fixed rates.

- If you’re thinking about buying an energy-efficient home with a Building Energy Rating (BER) of at least B3 or higher, you could apply for a green mortgage. You can learn more about green mortgages in this guide.

You can stay up to date on the latest mortgage news and helpful advice with our blogs and guides pages.

Get your mortgage with bonkers.ie

If you’re hoping to get your foot on the property ladder over the coming year, or are looking to save money by switching to a different lender, bonkers.ie can help you. We're more than just a comparison service!

With our mortgage broker service our team of experienced financial advisors here in Dublin can help you with your entire mortgage journey from application to drawdown.

We work with the country's top lenders so can find you the best mortgage rate for your particular circumstances and advise you on which lender is likely to offer you an exemption.

We can also apply to multiple lenders at the same time on your behalf, increasing your chances of getting approved for a mortgage, and saving you the time and hassle of having to apply to numerous lenders by yourself. We can also help you with getting mortgage protection and home insurance which are requirements for getting a mortgage in Ireland.

And the best news is that our service is entirely free and fully digital from start to finish, meaning everything can be done online from the comfort of your home! But don't worry, our team is only ever a phone call away if you need help or clarification on anything.