While discouraging, a mortgage refusal doesn’t mean you won’t be able to get approval in the near future.

Being refused a mortgage can be disheartening and can throw a huge spanner in the works if you’re trying to purchase a property.

However, it’s vital to understand the reasons behind your application rejection so that you know what to do if you want to apply again.

That’s why we decided to explore the nine main reasons why you could be refused a mortgage.

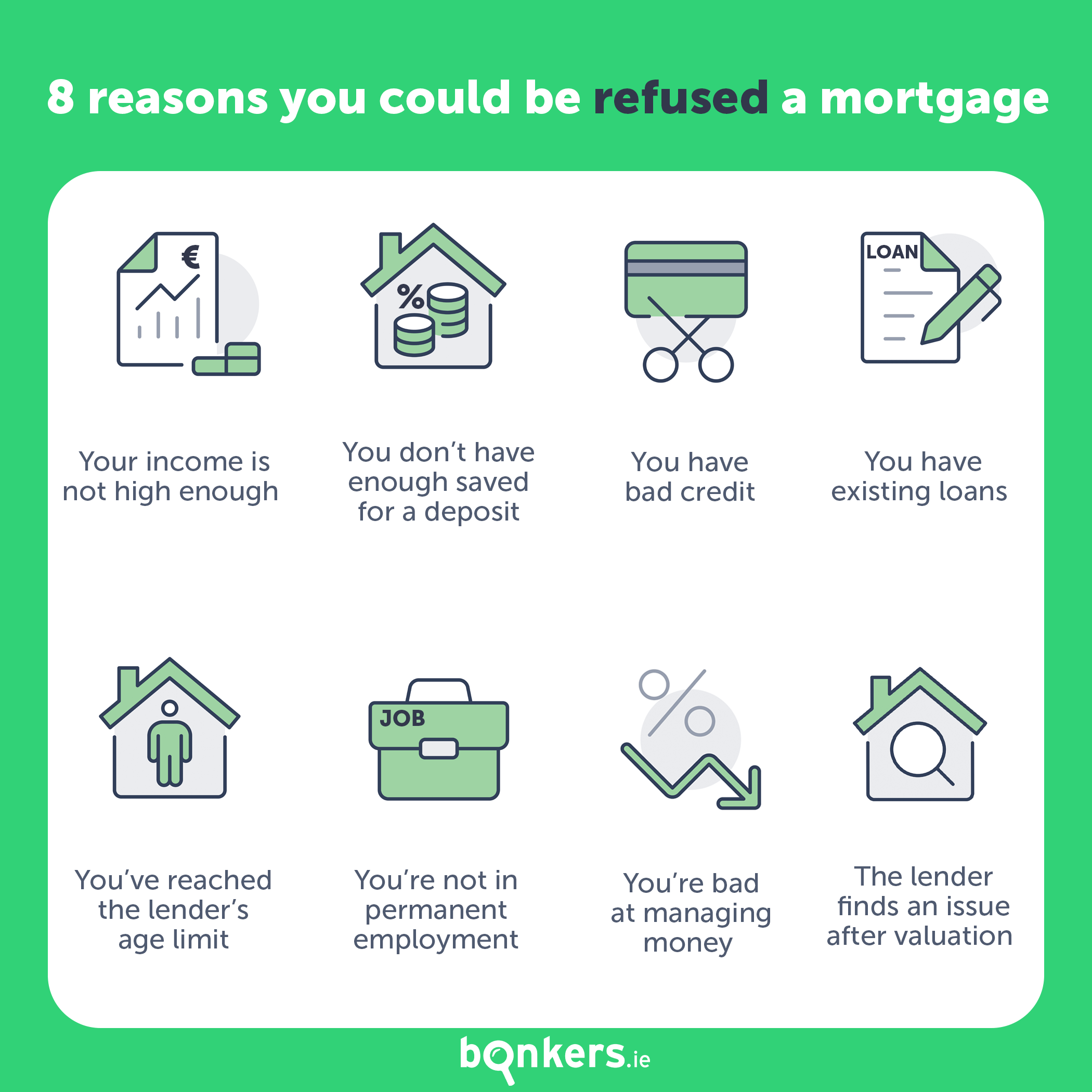

1. Your income is not high enough

It’s possible that your application was denied because your current income is not sufficient enough to repay the amount you wish to borrow.

Under the Central Bank’s mortgage lending rules, mortgage applicants are only permitted to borrow four times their gross annual income. This goes for both single and joint applicants.

For example, if you have a salary of €50,000, then the maximum mortgage you could be approved for is €200,000.

However, you may be eligible for a loan-to-income exemption. In any calendar year, lenders can offer an exemption to 15% of the mortgages they provide. Even still, lenders give out exceptions sparingly.

Take a look at our guide on the Central Bank’s mortgage lending rules to learn more.

2. You don’t have a full deposit

The second reason you could find yourself receiving a mortgage rejection is because you don’t have the minimum deposit required under the Central Bank of Ireland’s loan-to-value limits.

In Ireland, first-time buyers and movers are required to have a deposit of 10%.

However, you may be eligible for a loan-to-value exemption. This is when a lender reduces the deposit amount, so that instead you may be able to purchase the property with a smaller deposit.

Lenders can offer loan-to-value exemptions to 15% of mortgage applicants who may have a deposit of less than 10%.

3. You have a bad credit history

If you have a history of bad credit, you may struggle to obtain mortgage approval. This can happen if you didn’t pay off previous loans, or missed repayments in the past.

When you apply for a mortgage, a lender will run a check to view your credit history on the Central Credit Register (CCR). This report will show the lender your past and current credit commitments, and your capacity to manage and repay loans.

Your outstanding credit will help lenders assess your affordability, and can directly affect the amount you could borrow.

We’d recommend that you review your credit history before submitting a mortgage application.

If you need to improve your credit history consider:

- Paying off any arrears you may have

- Reduce the balance of your loan, credit card, or overdraft

- Try to avoid missing any repayments

- Don’t apply for new credit products

4. You have outstanding loans

Most people will need to take out a loan at one time or another throughout their life, whether it’s for a car, education, or a holiday. However, it’s a good idea to hold off on taking out a loan if you’re planning on applying for a mortgage in the near future.

This is because having other existing loans may hinder your ability to get a mortgage.

If you do have a hefty loan to repay, you could be refused mortgage approval. On the other hand, sometimes the amount you can borrow may just be reduced.

5. You’ve reached the lender’s age limit

Usually, lenders require borrowers to have paid their mortgage off by the time they’ve reached 65 or 70. This can cause difficulties for those looking to take out mortgages for longer durations, which can be up to 40 years with some lenders.

That means if you’re over the age of 40 and are applying for a mortgage, you’ll experience difficulty applying for a mortgage with a term of 30 years.

If this is the case, you can try to apply for a mortgage with a shorter term, if this is financially viable. Alternatively, you could apply for a smaller mortgage, over a shorter term.

6. You’re not in permanent, full-time employment

The way we work has changed drastically over the years and nowadays people tend to stay with the same employer for shorter periods of time and move around jobs more frequently.

While understanding of this, lenders need to be able to trust that you’re in a financially stable position so that you can meet mortgage repayments.

Lenders look more favourably at potential borrowers who are in permanent employment over contracted or temporary roles.

Typically lenders will require that mortgage applicants be in their current role for at least 6 months, and have passed their probationary period.

If you only recently started a job or your job is at risk, you could discover that your mortgage application has been rejected.

7. You’re bad at saving and managing money

If your bank statements show that you cannot save properly or that you have poor money management skills, you may struggle to obtain mortgage approval.

Similarly, if you have excessive gambling habits, your application will be frowned upon and you likely won’t receive approval. Gambling debts can accumulate fast and contribute to bad credit history. Lenders are wary when they see applicants sending money across to their betting account regularly.

If you want to better manage your money and savings, consider:

- Closing any gambling or online betting accounts

- Making a budget and setting aside a certain amount for savings each month

- Labelling all outgoings clearly, e.g. rent, savings, etc. so the lender can see where your money goes

- Cancelling any subscriptions you don’t use anymore

- Avoiding erratic spending

8. The lender finds an issue after the valuation

When purchasing a property, a lender will have its own independent valuation carried out on the property before agreeing to give you the mortgage.

This is to ensure that the property fits within its lending criteria and to check that the amount you’ll be paying represents the market value correctly.

If the lender thinks that the property isn’t worth what you’ve agreed to pay for it, they may decide to alter the amount they’re willing to let you borrow, or sometimes they will pull out completely. This is known as a down valuation.

If this happens, you could try to:

- Increase your deposit

- Renegotiate the price with the seller to meet in the middle

- Appeal against the valuation survey

- Apply for a mortgage with another lender

The lender may also refuse your application if other issues come to light when the property is valued, such as:

- Asbestos

- Damp

- Japanese knotweed

- Structural problems

- Roof problems

- Subsidence

Similarly, if the property is not of standard build, you may struggle to obtain mortgage approval.

9. You can't get mortgage protection or home insurance

In order to get a mortgage in Ireland, you need to have mortgage protection. This is a type of life insurance policy which pays off the outstanding balance on your mortgage in the event of your death.

You also need to have home insurance. If you can’t get either of these policies in place, your lender may refuse to allow you to draw down your mortgage.

Here are some of the reasons why you could be refused home insurance. And here's what to do if you are declined mortgage protection insurance.

What to do if you’ve been refused a mortgage

If you’re experiencing trouble with the mortgage application process we’d recommend that you speak to a mortgage advisor or broker, who will be able to help you get mortgage ready.

Local Authority Home Loan

If you have had two mortgage applications refused by lenders but you meet other certain criteria, you may qualify for a Local Authority Home Loan.

In January 2022, the Government announced this new mortgage scheme available to first-time buyers and Fresh Start applicants.

The scheme is designed for those looking to purchase new or second-hand residential properties and for self-builds. To qualify, you must provide proof of insufficient mortgage offers of finance from two regulated financial providers.

There are two fixed-rate loans available and the scheme has limits on the maximum market values of the property that can be purchased or built.

The loans are available through all local authorities nationwide.

Get your mortgage with bonkers.ie

If you’re hoping to get your foot on the property ladder over the coming year, or are looking to save money by switching to a different lender, bonkers.ie can help you. We're more than just a comparison service!

With our mortgage broker service our team of experienced financial advisors here in Dublin can help you with your entire mortgage journey from application to drawdown.

We work with the country's top lenders so can find you the best mortgage rate for your particular circumstances.

We can also apply to multiple lenders at the same time on your behalf, increasing your chances of getting approved for a mortgage, and saving you the time and hassle of having to apply to numerous lenders by yourself. We can also help you with getting mortgage protection and home insurance which are requirements for getting a mortgage in Ireland.

And the best news is that our service is entirely free and fully digital from start to finish, meaning everything can be done online from the comfort of your home! But don't worry, our team is only ever a phone call away if you need help or clarification on anything.