Keyperson insurance helps to protect one of the most important assets of a business or company - its people.

When it comes to protecting you and your family's future, there are plenty of insurance options available, such as life, health, serious illness cover, and mortgage protection and home insurance cover.

But there are also lots of important insurance options for businesses to consider too. One of which is keyperson insurance cover.

Taking out a keyperson insurance policy is not just for multinational organisations. It’s also a really important consideration for smaller businesses too, especially where one person is central to its success.

Before we get into the specifics of why keyperson cover might be important for you and your business, we should really start by asking the question...

Who is a keyperson?

A keyperson is any employee a company depends on for its continued success and whose death would cause the company to suffer an immediate financial loss.

Those considered ‘key’ are usually top-tier management such as directors, CEOs, and partners, but it can depend on the needs and wants of any particular business, ranging from cover for owners to managers, and so on.

What is keyperson cover?

In its simplest terms, keyperson insurance cover is a form of life insurance taken out by a company for an employee. The policy helps to protect the company’s financial interests and mitigate against any potential loss of earnings should a keyperson die while in the company's employment.

In the event of a keyperson passing away a lump sum will be paid out to help cover any expenses arising as a result of the keyperson’s death.

The policy associated with this type of insurance cover is usually a term assurance contract, with a term generally not exceeding the retirement age of the employee, although this can be negotiated separately with your insurance company.

Importantly, keyperson insurance is there to protect the company, is owned and paid for by the company, and is not the employee’s personal insurance cover.

What does keyperson insurance cover do?

Should a key employee die or become seriously ill, a business could suddenly be faced with mounting financial uncertainty as a result.

This could include anything from a disruption of management to a reduction in profits, even the loss of personal contacts known to the individual that could have been indirectly essential to the success of the business.

Taking out a keyperson insurance policy helps to safeguard your company or business should the worst happen. The payout provided after the death of the employee essentially buys your company time to find a new person or to implement other strategies to save the business.

Any costs that might arise during the recruitment process if a replacement was being sought for the keyperson would also be covered.

The policy can also be used to help repay any loans taken out by the insured. These can be loans guaranteed by the individual or personal loans made to the business from the employee.

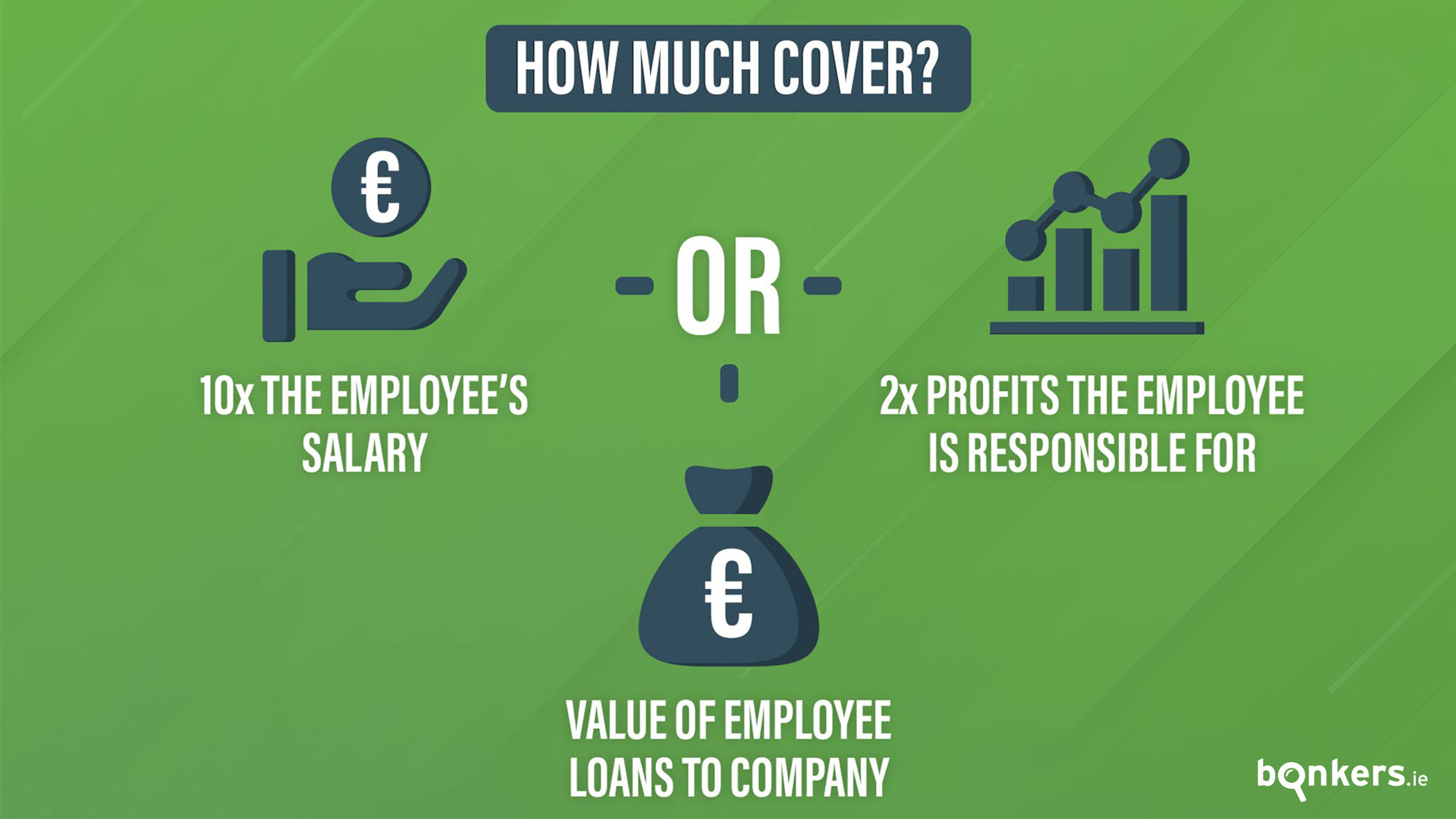

Deciding on how much cover you need

A key question any business, big or small, should consider when taking out keyperson insurance is what the estimated financial loss to your business would be if a key employee were to pass away.

The amount of cover you take out should equate to any potential loss of earnings that your business would suffer as a result of the keyperson’s death.

This will depend on each business or company's specific and ever-changing circumstances. However, as a general rule, it’s advisable to use a maximum of 10 times the person’s salary, or twice the gross profits the keyperson is responsible for.

As explained above, keyperson insurance can also be used to repay any loans the individual has personally guaranteed, or any loan made by the person to the company itself.

With this in mind, it’s possible to take out cover to match this value, ensuring any loans are paid off should the worst happen.

When taking out cover for an employee, businesses also have the option of adding Multi-Claim Protection Cover or serious illness cover to any policy. Adding serious illness cover means there will also be a payout if your employee gets seriously sick and cannot work.

Get cover in place with bonkers.ie

We know how difficult it can be to get the right level of cover in place at the right time, and at the right price, especially when it comes to protecting your employees.

At bonkers.ie we have our very own team of in-house insurance experts to help you and your business find the right cover for those you want to help protect.

We compare keyperson insurance cover across all of Ireland’s main insurance providers, helping you and your business to get the very best cover without the hassle of comparing all the options yourself.

To find out more, simply apply as normal using our life insurance comparison tool online.

Take a look at our other insurance guides

Did you find this guide helpful? If so, you might find our other insurance guides beneficial too!

- Learn all about life insurance in this guide and check out the answers to these 15 common life insurance questions.

- We mentioned specified illness cover in this guide. Here are 7 things to know before taking out specified illness cover.

- Discover simple ways you can reduce your insurance costs across a range of different insurance types so that you’re not overpaying.

You can stay up-to-date on all the latest insurance news and top saving tips with our blogs and guides.

Get in touch

Do you have any questions about being keyperson insurance? If so, don’t hesitate to contact us and we’d be happy to help. You can contact us on Facebook, Twitter or Instagram.