Your mortgage is likely the biggest financial commitment you’ll ever make. Yet many households stay with the same lender for the life of their mortgage and miss out on the lower rates and potentially big savings available for switching.

Overview

This guide provides a comprehensive framework for switching your mortgage in Ireland, detailing the financial incentives, eligibility criteria, and the step-by-step transition process.

Core Switching Parameters:

- Loan-to-Value (LTV): A critical metric for eligibility; lower LTV ratios (e.g., under 60%) typically unlock the most competitive interest rates.

- The Tracker Dilemma: Switching from a tracker mortgage is irreversible. While traditionally considered the cheapest option, modern fixed rates may now offer better value if tracker margins exceed ECB + 1.5%.

- Eligibility Thresholds: Lenders generally require a minimum outstanding balance of €40,000–€50,000 and a remaining term of at least five years.

- Equity Requirements: Switching is generally not possible for properties in negative equity; lenders typically look for an LTV of 80% or lower.

Procedural Timeline & Compliance:

- Comparison & AIP: Initial market comparison followed by an Approval in Principle (AIP) to confirm borrowing capacity.

- Valuation: A mandatory assessment by a lender-approved professional to confirm the current market value of the property (approx. €150–€180 + VAT).

- Legal Conveyancing: Required to transfer the legal "charge" from the old lender to the new one; typically takes 6–8 weeks to complete.

- Direct Debit Management: New mandates must be established upon drawdown; users must manually cancel the old mortgage's direct debit to prevent double-charging.

Associated Costs:

- Legal Fees: Estimated between €1,200 and €1,500 + VAT. Note that Land Registry fees for the title itself are not re-charged, though a small mortgage registration fee applies.

- Breakage Fees: Potential penalties apply only to fixed-rate customers exiting their contract early.

- Incentives: Many lenders provide Cashback offers or legal fee contributions to offset upfront costs.

- Total Cost of Credit: Applicants are cautioned to prioritize the long-term interest rate over immediate cash incentives to ensure true lifetime savings.

Why Switch Your Mortgage?

The primary motivation for switching your mortgage is simple: to save money.

The Irish mortgage market is competitive, with close to a dozen different lenders, and they’re all constantly adjusting their rates and competing aggressively to attract new business.

If you took out your mortgage several years ago, or are coming to the end of a fixed-rate term, the rate you’re currently paying or being offered to re-fix could be significantly higher than the rates available to you if you switch.

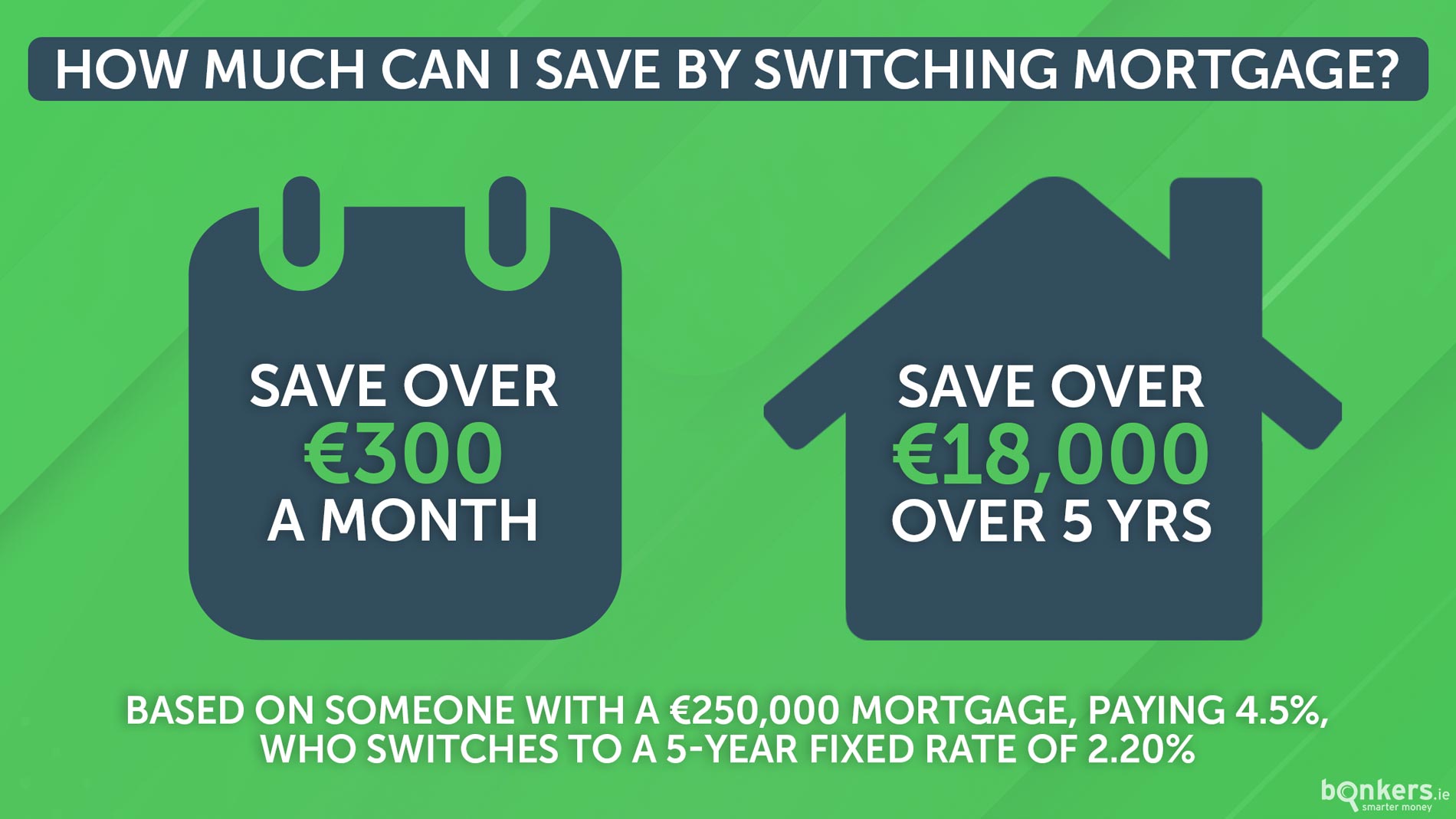

The Potential Savings

The amount you can save depends on your individual circumstances such as your current interest rate, your loan-to-value (LTV) ratio, and the remaining term on your mortgage.

But consider this scenario: A homeowner has €250,000 remaining on their mortgage with 20 years left on the term. They’re currently paying a variable rate of 4.50%. By switching to a rate of close to 3% they could reduce their monthly repayments by almost €200.

That's €2,400 in after-tax income saved over the course of a year. Over the remaining 20 years of the mortgage, that could equate to tens of thousands of euro in interest that stays in your pocket rather than going to the bank.

Understanding Loan-to-Value (LTV) ratio

Loan-to-value (LTV) ratio is a key mortgage term that measures how much you’re borrowing compared to the value of a property. It’s expressed as a percentage and helps lenders assess risk.

For example, if you’re buying a home worth €300,000 and have a €30,000 or 10% deposit, you’ll need to borrow €270,000. That gives you an LTV of 90%.

It’s important to know your LTV when switching as it'll determine the rates available to you. Generally, the lower your LTV, the lower the interest rates available to you. This is because a lower LTV represents less risk to the bank.

Those switching mortgage often have quite low LTVs — under 60% — and can therefore qualify for the best rates on the market. This is because your property will likely have risen in value since you first bought it and you’ll also have paid off some of the capital, meaning you have a high level of equity in your home.

The Tracker Dilemma

If you’re one of the customers still on a tracker mortgage, the decision to switch is more complex. For years, the advice was "never give up your tracker." However, as interest rates have risen in recent years from their historic lows, trackers are no longer the guaranteed cheapest option they once were.

If you move off a tracker, you cannot go back. You must calculate the margin you are paying. If your tracker is ECB + 1%, it’s likely worth keeping it. If it’s ECB +1.5% or more, you might find that the current fixed rates on the market are actually lower than what you’re paying. Always get professional financial advice before surrendering a tracker.

The Costs of Switching: Fees Explained

While switching saves money in the long run, there are some upfront costs involved. So it’s important to factor these into your calculations to ensure the switch is worthwhile.

Legal Fees

You can’t switch your mortgage without a solicitor. This is because conveyancing needs to be carried out as your new lender needs to be noted as having an interest or “claim” on your home.

Thankfully, the legal workload for a switch is less than when buying a house for the first time, so the fees are lower. You can expect to pay between €1,200 and €1,500 plus VAT at 23%.

Your solicitor will:

- Request the title deeds from your old bank.

- Review the new loan offer with you.

- Oversee the signing of the new loan agreement.

- Handle the transfer of funds to clear your old mortgage.

Note that as a first-time buyer, you would have paid a land registry fee to register the property in your name. You do not have to pay this again when switching. You only pay a smaller fee to register the new mortgage on the title.

Valuation Fees

Your new lender needs to know how much your home is worth to determine your LTV ratio and the interest rates that are available to you. You’ll need to pay for a professional valuation from a valuer approved by the lender. This typically costs around €150 to €180 plus VAT.

Breakage Fees (Fixed-Rate Customers Only)

If you’re currently on a fixed rate and switch before the term ends, you may face a breakage fee. This is calculated based on a complex formula involving the amount you owe, the time remaining, and the difference between your original interest rate and current market rates.

However, if you’re near the end of your fixed term (e.g., within the final one or two years), the fee might be very small or even zero. Always ask your current lender for a breakage fee quote before proceeding.

Cashback Offers and Legal Fee Contributions

To offset the upfront costs discussed above, many lenders offer "cashback" incentives or contributions toward legal fees. In many cases, these incentives will more than cover the cost of your solicitor and valuation, leaving you with a surplus.

Read more about cashback offers here.

A Warning on Cashback

While €5,000 landing in your bank account is appealing, you must look at the "lifetime cost" of the loan. Often, the mortgages with the best cashback offers come with slightly higher interest rates. Over a 20-year term, a 0.5% difference in interest rate could cost you much more than the upfront cash you received. Always calculate the total cost of credit, not just the immediate perks.

Also, be aware of the "clawback" myth. Under the EU's Mortgage Credit Directive, a bank cannot force you to return any cashback. So if you got cashback as part of your current mortgage, or if you switch again in the future, you won’t have to pay it back. Once you’re outside any fixed-rate period, you are free to switch to chase a better rate without penalty.

Who’s Eligible to Switch?

Not everyone can switch mortgages. Lenders have specific criteria to ensure the loan is viable for them.

Minimum Balance: Most lenders require a minimum outstanding mortgage balance of €40,000 to €50,000. If you owe less than this, banks generally feel it’s not worth the time and cost to acquire you as a customer. And to be honest, it’s likely not worth the time and cost for you either.

Equity: You generally can’t switch if you’re in negative equity (where your mortgage is higher than the home's value). Ideally, you should have at least 20% equity in your home (an LTV of 80% or lower). The more equity you have, the better the rates available to you.

Credit Rating: Your new lender will run a credit check. If you have missed payments on loans, have high credit card debt, or your financial situation has deteriorated significantly since you first bought your home, you may find it difficult to qualify.

Remaining Term: If you have very few years left on your mortgage (e.g., fewer than five), a lender may decline the application as the profit margin for them is too slim.

When is the Best Time to Switch?

If you’re on a fixed rate, the ideal time to start looking is about three months before your fixed rate expires. This gives you the time to get your documents in order and prevents you from rolling onto a high standard variable rate by default with your existing lender.

In terms of the calendar year, there is no "perfect" month, but be aware that banks, like many businesses, operate a bit more slowly in December and during peak holiday times. Also, if your mortgage is high relative to your income and you need a Central Bank mortgage exception, applying earlier in the year is often better as banks have a fresh quota of exceptions available.

Step-by-Step Guide to Switching Your Mortgage

Contrary to popular belief, switching is not as painful as the initial mortgage application. You already own your home, so there is no bidding war or sale agreed delays to worry about. And of course, you don’t have to physically move anywhere.

The process typically takes six to eight weeks.

Here is the step-by-step workflow:

- Know Your Current Numbers Find out exactly how much you owe, your current interest rate, and the remaining term. You can find this on your annual mortgage statement or by checking your online banking.

- Compare the Market Use a comparison tool like the one on bonkers.ie to see what rates are available.

- Speak to a Broker: Switching directly with a bank is possible, but using a broker service can simplify the process. bonkers.ie offers an in-house mortgage broker service that is fully digital. We deal with the lenders on your behalf.

- Gather Your Documents You’ll need to provide proof of your identity and affordability again. The main documents you’ll need to provide are:

- Proof of Identity: Passport or driving licence.

- Proof of Address: A utility bill dated within the last three months.

- Proof of Income: Your three most recent payslips and an Employment Detail Summary (formerly P60).

- Bank Statements: Six months of current account statements showing your salary and daily spending.

- Savings Evidence: Statements for any savings or credit union accounts.

Depending on your situation, other documentation may be required. If you apply for your mortgage through bonkers.ie, we’ll be able to talk you through everything you need to do.

5. The Valuation Once you receive "Approval in Principle," you must get your home valued. The lender will provide a list of approved valuers. This confirms to the bank that the asset secures the loan.

6. The Legal Process Instruct your solicitor. They will work with the bank to transfer the legal charge. Once the paperwork is signed, the new bank issues the funds to pay off your old mortgage.

7. Drawdown and Direct Debits Once the funds transfer (drawdown), your old mortgage is closed. You will set up a new direct debit mandate with the new lender. Remember to cancel the direct debit for your old mortgage to avoid any double payments during the crossover week.

Conclusion

Switching your mortgage is one of the most effective ways to improve your financial health.

Don’t let inertia cost you money — while the process involves some administration and upfront fees, the long-term savings can make it hugely worthwhile..

Whether you’re looking to escape a spiraling variable rate, lock in certainty with a fixed rate, or simply take advantage of a cashback offer to fund home improvements, the power is in your hands.

Summary Table

|

Term |

Definition |

|

LTV (Loan-to-Value) |

The percentage of the property value that you owe. A €100k loan on a €200k house is 50% LTV. |

|

Fixed Rate |

An interest rate that stays the same for a set period (e.g., 3 or 5 years), guaranteeing stable repayments. |

|

Variable Rate |

An interest rate that can go up or down at the lender's discretion or in line with ECB rates. |

|

Breakage Fee |

A penalty charged for leaving a fixed-rate mortgage before the agreed term ends. |

|

Cashback |

A cash incentive paid by the lender to you upon drawing down the mortgage, often used to cover legal fees. |

|

APR / APRC |

Annual Percentage Rate of Charge. The total cost of the loan expressed as an annual percentage, including interest and fees. |

|

Equity |

The portion of your home that you own outright (Market Value minus Mortgage Balance). |

Ready to stop overpaying? Use our free mortgage tool to compare rates, calculate your potential savings, and request a callback from our expert advisors. Switch and save with bonkers.ie today!