Take control of your mortgage journey today. Compare interest rates, cashback offers, and green incentives across all lenders on bonkers.ie to find the deal that saves you money.

Overview

This guide analyses how to optimise your mortgage strategy by balancing immediate incentives against long-term financial health. We break down the mathematics of interest rates and the specifics of energy-efficient lending

Key Decision Drivers:

- Cashback vs. Interest Rates: While upfront cash (typically 2%–3%) helps with immediate costs like furnishing, these products often carry higher interest rates. Over a 30-year term, the extra interest paid can far exceed the initial cash windfall.

- Green Mortgages: Properties with a Building Energy Rating (BER) of B3 or higher qualify for "Green Rates." These are often the lowest rates on the market, though they are usually restricted to fixed-term contracts and may exclude cashback eligibility.

- The "Switcher Hack": Under EU law, lenders generally cannot "claw back" cashback if you switch after your fixed term ends, allowing savvy borrowers to take the cash and move to a lower rate later.

Introduction

Buying a home is one of the most significant financial milestones in your life, but it is also one of the most expensive. Once you have navigated the stress of bidding wars and solicitor fees, you are faced with a dizzying array of mortgage products. Do you take the lump sum of cash now to help furnish the house? Do you opt for a lower interest rate to save money over thirty years? Or do you focus on the energy efficiency of your property to unlock special "green" discounts?

To make matters even more complex, once you have the mortgage, you then have to decide how to manage it. If you come into some extra money, should you pay down your debt or invest it in a pension?

At bonkers.ie, we believe in breaking down complex financial jargon into plain English. We have analysed the market to bring you a complete guide on mortgage cashback, green rates, and repayment strategies. Our goal is to move you from confusion to clarity, helping you choose the product that suits your wallet, both for today and for the decades to come.

The Mortgage Dilemma: Cashback or a Lower Rate?

For many buyers, especially those stretching themselves to get on the property ladder, cash is king. When you have spent your savings on a deposit, stamp duty, and valuation fees, the bank account can look a little empty. This is where mortgage cashback offers shine.

How Cashback Works

Cashback is exactly what it sounds like: a lender gives you a percentage of your mortgage back in cash shortly after you have drawn down the loan.

The trend was kicked off by Bank of Ireland back in 2015 and has since been adopted by various lenders to attract customers. The amounts can be substantial. For example, on a €300,000 mortgage, a 2% cashback offer puts €6,000 directly into your bank account. That is money for a new sofa, a dining table, or perhaps to replenish your emergency fund.

However, you must look beyond the initial financial incentive. Lenders offering significant cashback often charge higher interest rates than those who do not.

The Long-Term Cost of Short-Term Cash

It’s important to treat a cashback offer as a mathematical equation rather than a free gift. If you accept a higher interest rate in exchange for cash upfront, you could end up paying significantly more over the life of the loan.

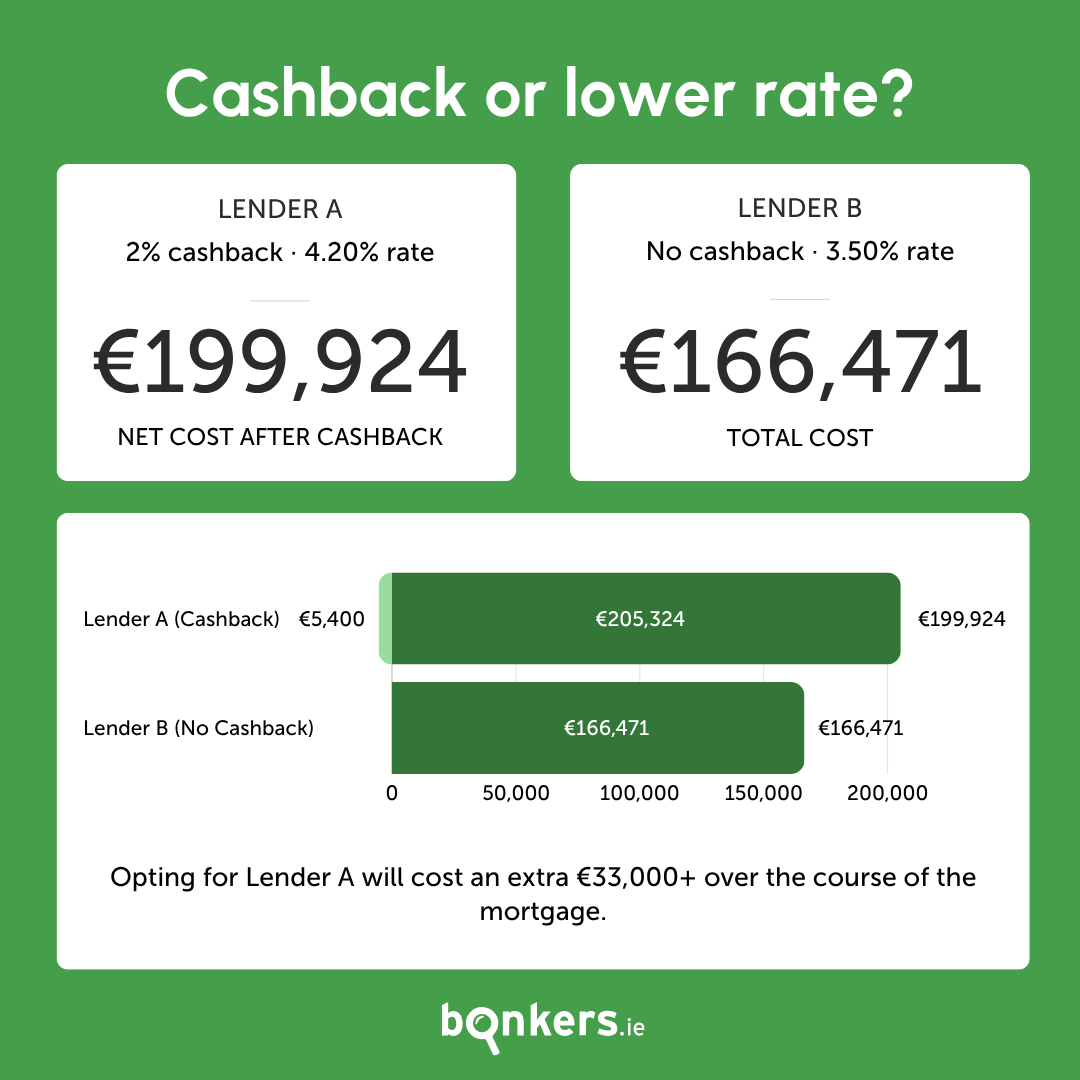

Consider this scenario: You take out a €270,000 mortgage over 30 years.

- Lender A offers 2% cashback (€5,400) but charges a rate of 4.20%. The total cost of credit over the lifetime of the loan is roughly €205,324. Even after subtracting the free cash, your cost is roughly €199,924.

- Lender B offers zero cashback but a lower rate of 3.50%. The total cost of credit here is just over €166,471.

In this example, taking the cashback initially looks like a win, but it effectively costs you over €33,000 in extra interest payments over the mortgage term.

The Switcher Strategy

There is a "hack" to this system, but it requires diligence. Under the EU’s Mortgage Credit Directive, banks cannot claw back the cash incentive if you switch lenders later.

This means you could technically take a cashback offer, stay for a few years, and then switch to a lower-rate lender. However, if you are on a fixed rate, you may face a "breakage fee" for leaving early.

The strategy here would be to take a short-term fixed rate (e.g., three years), enjoy the cash, and switch immediately once the fixed term ends. If you are not the type of person who stays on top of financial administration, the "set and forget" lower rate might be safer.

Green Mortgages Explained

As the world focuses on sustainability, lenders have introduced "green mortgages" to incentivise energy-efficient homes. But what does this actually mean for you, and is it just a marketing spin?

What Is a Green Mortgage?

A green mortgage offers a lower interest rate to borrowers buying a home with a high energy efficiency rating. To qualify, the property usually needs a Building Energy Rating (BER) of B3 or higher.

Since 2019, all new builds in Ireland generally require an A2 rating by law, meaning almost every new home qualifies automatically.

However, this product is also available to switchers or those buying second-hand homes that have been retrofitted to meet the B3 standard.

The Financial Benefit

The discount can be substantial. For instance, AIB has offered green rates significantly lower than its standard rates, sometimes a difference of over 1% on fixed terms. On a large mortgage, this reduction saves you thousands of euro annually, far outweighing the benefits of a one-off cashback sum in many cases.

Bank of Ireland takes a slightly different approach with an "EcoSaver" model, offering a sliding scale of discounts based on the BER. The better the rating (from G up to A), the better the discount.

Is It Greenwashing?

There is a debate regarding whether these mortgages actually help the environment. Critics argue this is "greenwashing" — a known marketing tactic to look eco-friendly without driving real change. Since new homes must be energy-efficient by law, the bank isn't necessarily causing the home to be built; they are just financing it.

Furthermore, green mortgages are rarely "green" in terms of how the bank funds them (i.e., not necessarily backed by carbon offsets). However, for the consumer, the debate is secondary to the savings. If you are buying an energy-efficient home, you should absolutely avail of the lower rate.

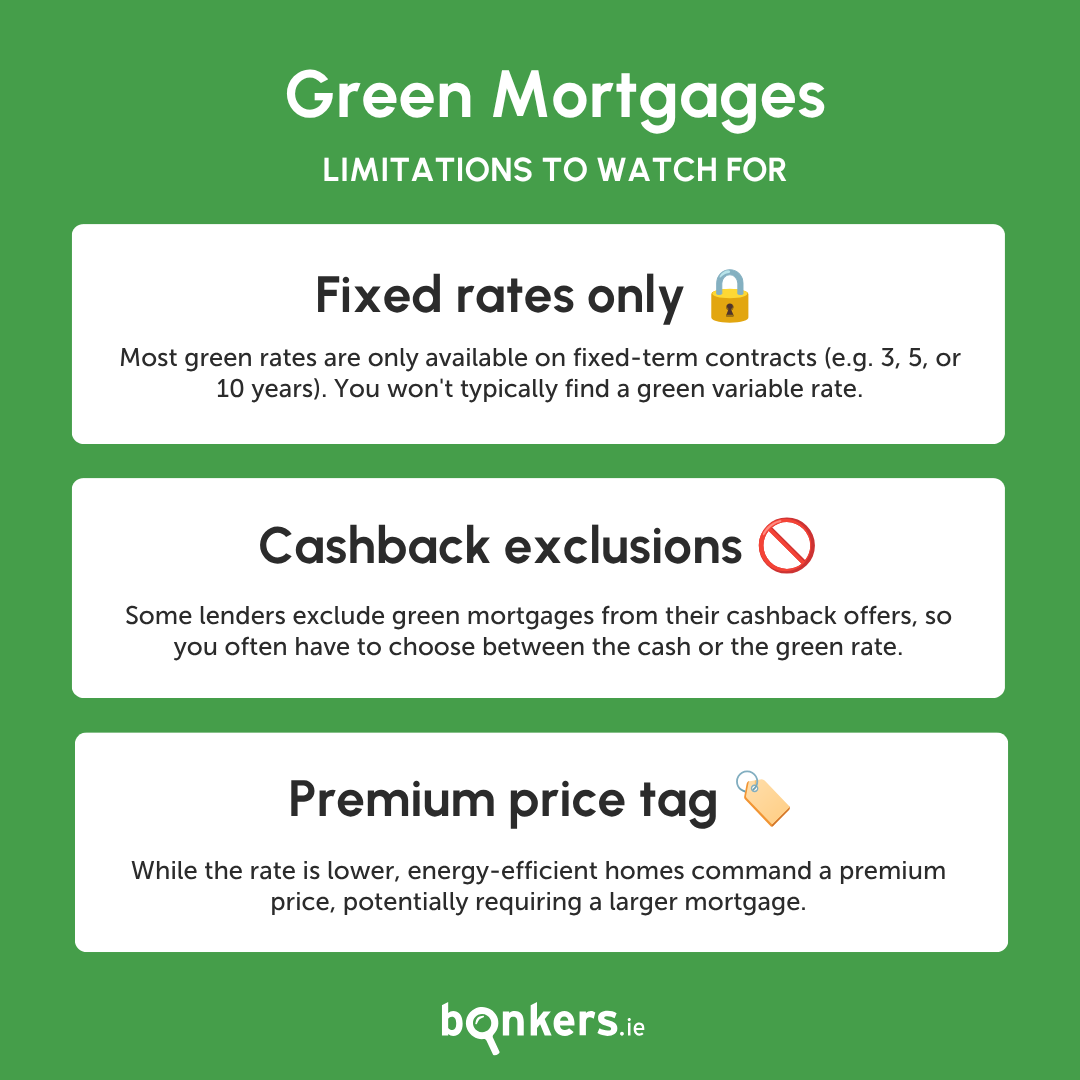

Limitations to Watch For

Before you commit to a green mortgage, check the fine print:

- Fixed Rates Only: Currently, most green rates are only available on fixed-term contracts (e.g., 3, 5, or 10 years). You won't typically find a green variable rate.

- Exclusions: Some lenders exclude green mortgages from their cashback offers. For example, Haven has excluded its green four-year fixed rate from its cashback scheme. You often have to choose between the cash or the green rate.

- The Premium Price Tag: While the rate is lower, the house itself might be more expensive. Energy-efficient homes command a premium price, potentially requiring a larger mortgage overall.

Conclusion

Choosing the right mortgage product is a balancing act between your immediate needs and your long-term financial health.

Cashback offers can provide a lifeline for furnishing a new home, but they often come with higher interest rates that cost significantly more over time. If you are organised enough to switch lenders after the cashback period, you can beat the system, but it requires effort.

Green mortgages offer a fantastic way to access lower rates, provided your home meets the BER criteria. However, you often have to sacrifice cashback incentives to access these eco-friendly rates.

Finally, while the dream of being mortgage-free is powerful, do not rush to pay off your loan at the expense of your liquidity or pension planning. Ensure you have an emergency fund and are maximising your tax-free pension contributions first.

There is no "one size fits all" answer. The best approach is to compare the market thoroughly. Look at the total cost of credit, not just the introductory offer.

Summary Table

|

Feature |

Cashback Mortgage |

Green Mortgage |

Low Rate (Non-Cashback) |

|

Primary Benefit |

Lump sum cash upfront (1% - 3%) |

Lower interest rates |

Lowest overall cost of credit |

|

Best For |

First-time buyers needing cash for furniture/fees |

Buyers of A/B3 rated homes |

Long-term savers focused on total cost |

|

Downside |

Usually higher interest rates |

Strict BER criteria required |

No cash lump sum to help with moving |

|

Switching Rules |

Can switch after term (watch breakage fees) |

Usually fixed-term contracts |

Easier to switch if variable |

|

Environmental |

No specific requirement |

Requires BER B3+ (usually) |

No specific requirement |

Ready to find your best deal? Compare interest rates, cashback offers, and green mortgages quickly and easily on bonkers.ie today.