Five years ago, if you had a few bob and nerves of steel, you could have done your bit for country and economy by putting your money into almost any kind of deposit account with one of the many ailing Irish banks. And goodness knows, the banks sure needed the money.

It would have been quite an act of patriotism. You’d have shown that you didn’t believe there would be a Cypress style write down or an Icelandic run on the banks. You’d have shown belief that our government wouldn’t see you short on your savings and you’d actually get your money back. With white knuckles you’d have put your faith in Brian Cowan’s vision and leadership and held on tight.

And in fairness, the reward for such patriotism could be pretty good back in the day.

High interest

Five years ago you could get nearly 5% on a short term account from Permanent TSB, 6% if you were prepared to put your money on deposit with Anglo Irish Bank for just one year, and an unbelievable 7% on a regular saver from Bank of Ireland.

There were actually plenty of wild new high-interest accounts around in 2009 which is hardly surprising really. Anglo was nationalised in January that year which was followed swiftly by the resignation of such notables as Patrick Neary and Michael Walsh (remember them?). Five years ago, the banking crisis was in full swing and people were not putting money into Irish banks, they were taking it out by the cartload.

So much so that Brian Lenihan had to whiz about the place assuring the nation that he had it all in hand, while at the same time he was handing billions to the banks as part of the recapitalisation scheme.

The people were seriously worried about their money too. They were worried that their savings would be wiped out so people were looking for somewhere safe to put their money. It’s why savings rates were so high in most banks… but not all.

Safe

Instead of hiking rates to match the big banks, the likes of RaboDirect and NationwideUK took a more sober approach to attracting cash. “A safe haven for your savings” said NationwideUK and “Ireland's Only AAA Rated Bank so we promise your money is safe!" said RaboDirect.

The sensible and safe messages worked. People who’d never been on the internet before were suddenly opening accounts in banks with no branches, and beaming money into new accounts with guarantees from countries like Holland and the UK.

You couldn’t get huge interest rates at these banks though. It wasn’t what they were selling. While Anglo Irish Bank was offering a spectacular 4.75% AER on their Demand account(!), RaboDirect was only offering 2.0% to their demand customers.

Long term

But if you were prepared to sock your money away for a very long time, you could do very well indeed with some of the internet and overseas banks. RaboDirect were happy to acknowledge it too. “What we currently have to offer in terms of short term deposits probably isn’t going to rock your world!” they said back then, “…unless you’re looking to lock your money away for say, 3 to 5 years.”

On a five year term with RaboDirect back in 2009, you could get 4.05% AER. When you compare that to the 1.40% you’ll get on the same account today, you can see just how strong that rate was. And of course people signed up. They wanted somewhere Triple A safe for their savings while they waited for the mayhem to die down. If it meant putting money away for the long term, so be it - and a nice interest rate would do just fine too.

I bring this up because we are now hearing from people that did actually put money away for the long term during the crisis. People who's accounts are now reaching maturity and many of them are not happy…

And here’s why… Let’s say you put €30,000* into that RaboDirect five year term account back in March 2009. You’d have locked in a very nice fixed rate 4.04% AER for the whole term. That should yield around €6,500 in interest for your troubles. A terrific return altogether.

DIRT

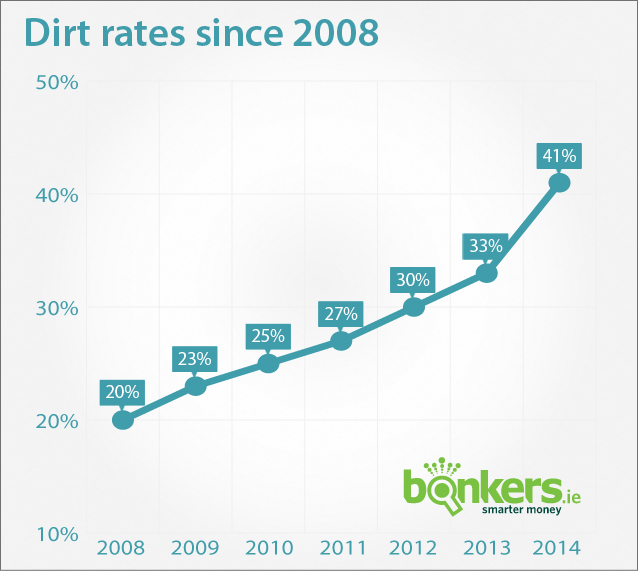

You wouldn’t get all of that of course. There’s DIRT to consider and back then the two Brians had just hiked the DIRT rate from 20% to 23%. Not a huge hike, but 23% would still peel nearly €1,500 off your return leaving you with €5,005. Still, not bad, a grand a year is nothing to be sniffed at and people back then probably expected that they’d actually get that at the end of their term.

But here’s where the story takes a turn. Seeing the kind of readies that could be made from taxing peoples’ savings, the last couple of Finance Ministers kept pushing the DIRT rate up in every budget until last October Michael Noonan gave it an almighty shove to 41%. So now more than two fifths of every euro earned in interest goes straight to the government.

And that’s why our term deposit customers are so unhappy. Instead of getting €6,500 in interest, or even €5,000; when their five year terms actually do mature, they’ll get just €3,800. There’s no provision for the fact that DIRT was 23% in 2009 or 27% in 2011. Customers with term accounts maturing now will all be hit with a flat 41% on all their interest - even if it's calculated annually and paid on maturity. And that's why some of the folks that had faith back in 2009 feel as though they've been roasted.

*I've used €30,000 as the deposit amount because back in 2009 that was actually just shy of the average amount on deposit per household in Ireland.